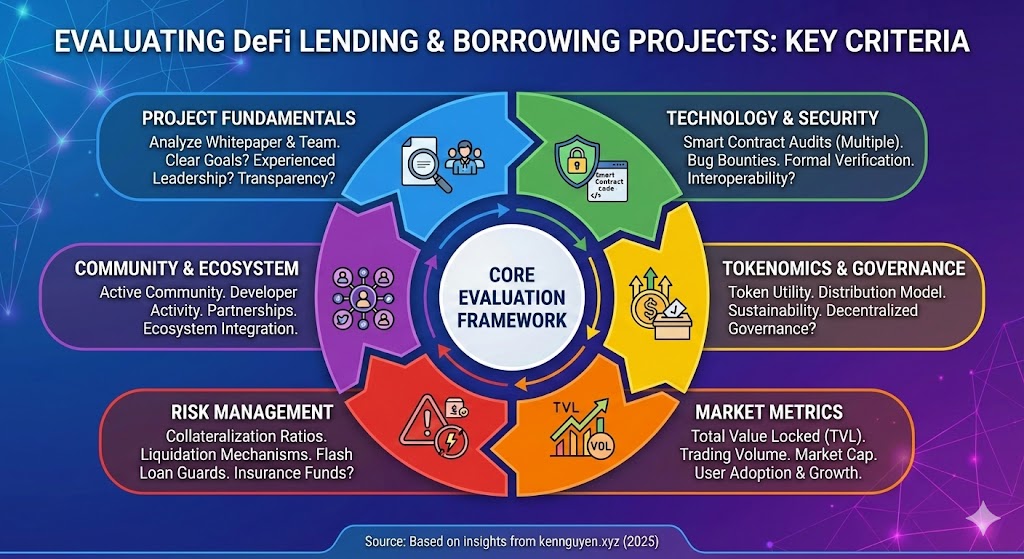

Evaluating DeFi Lending and Borrowing Projects

Decentralized finance (DeFi) has fundamentally changed how people access financial services, especially lending and borrowing. Instead of relying on banks, anyone can lend liquidity or borrow assets using smart contracts.

But the opportunities come with serious risks: smart-contract failures, protocol insolvency, liquidity crises, governance attacks, stablecoin depegs, and economic exploits.

To navigate this landscape safely, you need a structured framework to evaluate DeFi lending/borrowing platforms before committing your capital. This guide breaks down the most important criteria, explains what to look for, and includes practical tools and red flags.

1. Smart-Contract Risk: The #1 Cause of Losses

Why it matters

A flawed smart contract can result in permanent loss of funds. Many DeFi losses come from reentrancy attacks, oracle manipulation, flash-loan exploits, and logic bugs.

What to evaluate ️✅

✔ Audit quality—not just existence

- Look for well-known auditors like OpenZeppelin, Trail of Bits, Certora, ChainSecurity, Sigma Prime, PeckShield.

- Read the audit reports: Were critical issues found? Were they fixed?

✔ Formal verification

Protocols like Aave and Compound use formal verification tools (Certora, Slither). This significantly reduces risk.

✔ Bug bounty program

A strong program (via Immunefi or GitHub bounty) with high payouts signals seriousness.

✔ Time in production

A contract with 2+ years of exploits-free operation is more trustworthy than a newly deployed one.

Red flags 🚩

- Only low-tier auditors or no audit at all

- Recently deployed smart contracts (<6 months)

- No public audit reports

- No bug bounty program

2. Protocol Architecture & Collateral Model

DeFi lending protocols typically use one of these models:

A. Overcollateralized pools (e.g., Aave, Compound)

- Borrowers deposit collateral > loan value

- Safer and more battle-tested

- More predictable liquidation mechanics

B. Isolated lending markets (e.g., Venus Isolated Pools, Aave Isolation Mode)

- Contains risk by preventing cross-asset contagion

- Ideal for newly listed or volatile assets

C. Under/uncollateralized lending (e.g., Maple, Clearpool)

- Much riskier—relies on credit assessment or institutional borrowers

- Higher APY but higher chance of defaults

Evaluate liquidation mechanisms ️✅

An effective DeFi lending protocol needs:

- Real-time collateral monitoring

- Healthy liquidation incentives (5–12% typically)

- Efficient auction systems or third-party liquidators

- Robust price-oracle integration

Red flags 🚩

- Accepts highly volatile assets as collateral

- Weak liquidation incentives

- Liquidity is too low to support liquidations during volatility

3. Oracle Reliability

Why it matters

Price oracles determine whether a loan is safe or liquidated. Incorrect prices can lead to mass liquidations or under-liquidation.

Best-in-class oracle practices ✅

- Chainlink price feeds (widely considered safest)

- Multiple oracle sources + fallback mechanisms

- Time-weighted average prices (TWAP) for volatile assets

- Rate limits on price updates to prevent flash-loan manipulation

Red flags 🚩

- Native/or custom oracles with no track record

- Relies solely on DEX price for volatile assets

- Oracle update frequency too slow or too fast

4. Tokenomics & Incentive Sustainability

Many DeFi protocols attract liquidity using high APY rewards. But suspiciously high yields can signal high risk.

Evaluate sustainability ✅

- Organic yields (funded by borrowers paying interest)

- Low reliance on inflationary token emissions

- Healthy utilization ratio (usually 60–80%)

- Diversified revenue streams (origination fees, liquidation fees, flash-loan fees)

Analyze protocol token usage

- Does the token have real utility (governance, insurance, staking)?

- Is it required for borrowing/lending?

- Are emissions decreasing over time?

Red flags 🚩

- Rewards > 20–30% APY without real revenue backing them

- Ponzi-like emissions with no long-term plan

- Yield that comes only from the protocol’s native token

5. Liquidity Depth & Market Health

A lending protocol is only as safe as its liquidity.

Metrics to analyze ✅

✔ Total Value Locked (TVL)

Higher TVL = better liquidity, stronger safety.

✔ Asset distribution

Look for concentration risk. If 60% of liquidity is one asset, the protocol may be fragile.

✔ Borrow utilization

Healthy = 60–85% Danger = >90% (withdrawals may fail)

✔ Supply/borrow growth trends

Stable growth = organic adoption Sudden spikes = mercenary liquidity chasing rewards

Tools to check

- DeFiLlama

- Dune Analytics dashboards

- Token Terminal

Red flags 🚩

- Sudden drop in TVL (may signal problems)

- Extremely high utilization (>95%)

- Very low liquidity for major assets

6. Team Transparency & Governance

Even decentralized protocols rely on human oversight.

What to look for ✅

✔ Docs and transparency

Clear documentation, public multi-sig addresses, protocol analytics, and governance records.

✔ Responsible governance

- Decentralized voting with checks & balances

- Transparent treasury usage

- Public development roadmap

✔ Reputation & history

Reputable teams (Aave, Maker, Compound, Silo, Frax) have long track records and audits.

Red flags 🚩

- Anonymous team + complex protocol = high risk

- Governance controlled by a small number of wallets

- No documentation or clear roadmap

7. Asset Risk: The Importance of Choosing Good Collateral

Even if the protocol is safe, the assets you deposit might not be.

Safe collateral characteristics ✅

- High liquidity

- Large market caps

- Long trading history

- Well-integrated in DeFi

Examples:

- ETH

- WBTC

- Stablecoins (USDC, DAI, USDT)

Avoid risky assets as collateral 🚩

- Illiquid tokens

- New governance tokens

- Algo stablecoins (e.g., UST-like risks)

- Meme coins (no price floor)

Even in reputable protocols, assets like these get liquidated rapidly or experience oracle manipulation.

8. Stablecoin Risk: Critical for Lending Markets

Most DeFi credit systems revolve around stablecoins.

Evaluate stablecoin reliability ✅

- Backing transparency

- On-chain vs off-chain collateral

- Regulation risk

- Minting/redemption mechanisms

- Historical depegs

Stablecoins to favor: USDC, DAI, USDT

Be cautious of:

- Algorithmic stables

- Low-liquidity new stablecoins

- Overcollateralized stables with exotic collateral (e.g., protocol tokens)

9. Economic Security & Stress Testing

Strong protocols simulate worst-case scenarios:

✔ Stress test tools

Aave Risk DAO and Gauntlet provide real-time simulation of market crashes.

✔ Historical performance

Check how the protocol behaved during:

- 2020 market crash

- 2022 Terra/Luna collapse

- 2022 FTX implosion

- 2023 USDC depeg

If it survived all of these, it’s battle-tested.

10. Community Sentiment & Reputation

Even if everything looks perfect on-chain, community signals matter.

✔ Check:

- Discord and Telegram activity

- Developer communication

- Transparency during incidents

- Community trust level

✔ Look for:

- Consistent updates

- Fast response to security issues

- Honest reporting

Red flags 🚩

✖ Dead community ✖ Censored discussions ✖ No updates for months

TL;DR: A Practical Checklist

Before using a DeFi lending/borrowing project, verify:

Security

- High-quality audits

- Long uptime history

- Strong oracles

- Active bug bounties

Financial health

- Organic yields

- Sustainable tokenomics

- Healthy liquidity

- Good utilization ratio

Governance

- Transparent documentation

- Decentralized governance

- Responsible treasury usage

Asset-level risks

- Use liquid, stable collateral

- Avoid volatile or illiquid tokens

- Prefer established stablecoins

Conclusion

Evaluating DeFi lending/borrowing projects is about understanding both technical risk and economic risk. No project is 100% safe, but using a structured framework dramatically reduces the chance of catastrophic losses.

If you’re disciplined about evaluating smart-contract security, liquidity depth, stablecoin reliability, and protocol governance, you can capture the opportunities in DeFi while minimizing downside.