Crypto and the Money Supply

For all the narratives surrounding crypto, like decentralization, innovation, revolution, the uncomfortable truth is that digital assets are, at their core, reflections of global liquidity.

Their cycles, booms, and busts trace the same contours as the broader monetary landscape. In other words, crypto is just a mirror held up to the money supply.

This relationship has become even clearer in recent years as markets transitioned from the era of quantitative easing (QE) to quantitative tightening (QT). While Bitcoin and other digital assets were once seen as independent or even oppositional to central banks, their performance now moves almost lockstep with liquidity conditions.

To understand where crypto might go next, one must look less at whitepapers and roadmaps, and more at the Federal Reserve’s balance sheet.

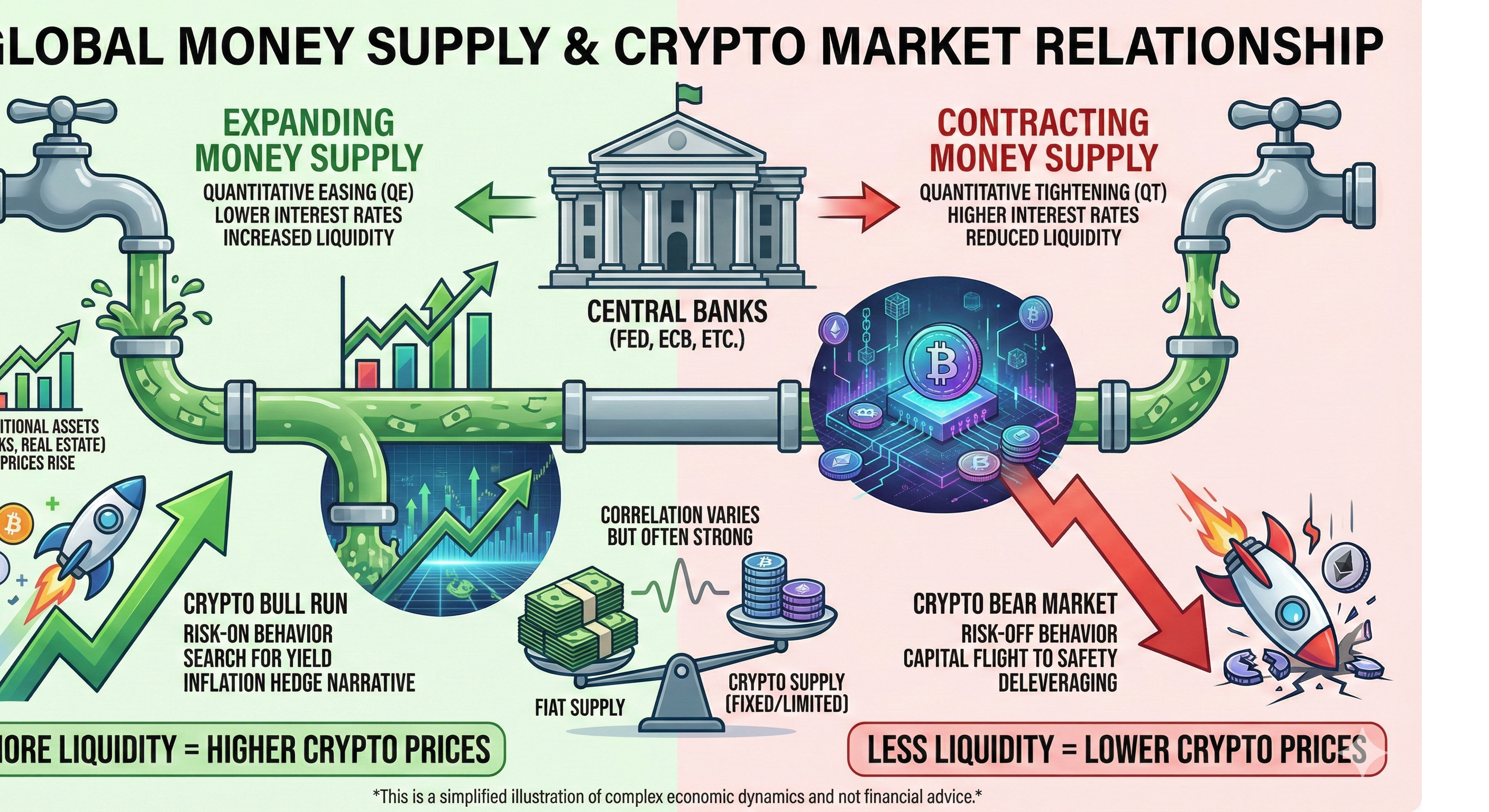

The Liquidity Engine That Drives Everything

Let’s start with the basics: in a world driven by fiat currency and credit expansion, liquidity is the lifeblood of risk assets. When central banks inject liquidity through QE, expanding their balance sheets by purchasing government or corporate bonds, that new money doesn’t just sit idly in the system. It flows outward, seeking returns.

In times of easy money, speculative assets thrive. Venture capital booms. Tech stocks soar. And crypto, as perhaps the highest-beta asset class in existence, goes parabolic.

The 2020–2021 cycle was a textbook case: central banks unleashed unprecedented liquidity to combat COVID’s economic fallout, and Bitcoin surged from under $10,000 to over $60,000. Ethereum followed. Altcoins exploded. NFTs became a cultural phenomenon.

But when the tide turns, when central banks pivot from QE to QT, the effects ripple instantly through every layer of the market. Liquidity is withdrawn. Risk appetite collapses. Prices deflate. The 2022–2023 bear market wasn’t about “bad projects” or “regulatory FUD” alone, it was a macro liquidity contraction, plain and simple.

We’re Still in QT, and Crypto Feels It

Today, global liquidity remains tight. Central banks are still draining balance sheets, interest rates remain elevated, and dollar liquidity is constrained. For crypto investors hoping for another bull run, this is the invisible ceiling.

As long as QT persists, there simply isn’t enough marginal liquidity to chase speculative returns. The flows that once bid up meme coins and high-beta tokens are now content sitting in money market funds earning 5% risk-free.

When the system is prioritizing safety and yield, the risk curve compresses, and crypto sits at the very end of that curve.

This doesn’t mean crypto is dead. It means the macro backdrop doesn’t support expansion yet. Until the money printer reverses course, or liquidity injections resume in some form, the crypto market will remain a reflection of contraction.

Bitcoin Is Graduating From “Crypto”

That said, it’s time to start drawing a line between Bitcoin and the rest of the crypto complex.

For years, Bitcoin was lumped together with every altcoin under the “crypto” umbrella, a messy catchall that included everything from DeFi experiments to outright Ponzi schemes.

But the landscape has changed. The approval of Bitcoin ETFs in the U.S., the entrance of institutional investors, and the embrace of Bitcoin as a macro asset have fundamentally altered its identity.

Bitcoin is no longer just “crypto.” It’s becoming part of the legitimate global financial system, a hard, digital asset that institutions can hold alongside gold, equities, and bonds. It has survived multiple cycles, regulatory crackdowns, and narrative shifts. It’s integrated into traditional custody solutions, trading desks, and portfolio models.

Ethereum and the broader altcoin ecosystem, meanwhile, remain deeply tied to speculative flows and venture-style risk. Their valuations are still primarily a function of liquidity, not adoption or cash flow. That distinction matters. Bitcoin is increasingly macro; crypto is still micro.

The Next Wave Depends on the Fed

The idea that crypto exists outside the traditional financial system has always been more myth than reality. In truth, digital assets are expressions of the same liquidity dynamics that move stocks, bonds, and real estate.

The blockchain may be decentralized, but its price action isn’t immune to the central bank’s balance sheet.

Right now, as the world remains in quantitative tightening, the liquidity simply isn’t there to fuel another speculative boom. But when conditions shift, when liquidity returns, the next chapter will look very different. Bitcoin, now institutionalized and legitimized, will likely serve as the anchor. The rest of crypto will continue to dance in its shadow.

In the end, crypto doesn’t escape the system. It reflects it.